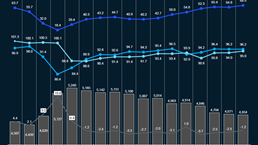

Brent crude oil prices decreased in April to an average of USD68.1/bbl m-o-m, a decline of USD4.6/bbl compared to the previous month’s average. Oil prices in April 2025 were at their lowest point since May 2021, driven by uncertainty over the OPEC+ production increase and continued US tariff dispute, which has eroded the fuel demand outlook:

- Global oil demand. Global liquids demand decreased marginally in April by 0.3 MMb/d m-o-m to 103.6 MMb/d. The minor increase in demand from China and India was offset by similar levels of demand decline in Japan and the Middle East

- OPEC 9 production (excl. Iran, Venezuela, Libya). OPEC 9’s production remained relatively stable, witnessing a marginal decline of ~0.2 MMb/d to 27.2 MMb/d in April, with no single country contributing to significant change. Eight OPEC+ members have agreed to speed up their production output hike, planning to increase cumulative volumes by ~0.4 MMb/d during May

- Non-OPEC production (excl. US shale). Non-OPEC production remained the same m-o-m at 61.9 MMb/d. Production declines in Canada, Kazakhstan, and China were offset by production increases in the US and Brazil

- US shale oil production. US shale production levels remained virtually the same m-o-m, averaging at 9.2 MMb/d in April. The number of active rigs stood at 566 during April, down by three units compared to March 2025

- Iran, Venezuela, Libya production. Combined production levels in Iran, Venezuela, and Libya averaged at 5.5 MMb/d during April 2025, with none of the countries showing a significant change in volumes

- Commercial inventories.1 Global commercial inventories increased by ~32 million barrels in April, driven by an increase in non-OECD inventories. Overall, inventories have remained relatively steady at ~4.5 billion barrels over the last six months

- Market sentiment. Brent prices fell in April after eight OPEC+ members, led by Russia and Saudi Arabia, announced plans to expedite an unwinding of oil production cuts starting in May. The ongoing tariff war between the US and several other countries had already introduced uncertainty in the oil demand outlook, driving prices lower, but now with the OPEC+ unwinding cuts, the risk of oversupply is escalating

1 Non-OECD share of inventories is estimated, assuming that non-OECD inventories have 50% days of demand cover of OECD inventories

Download dashboard:

Oil supply & demand dashboard: April 2025

Subscribe to Energy Solutions

To receive our oil supply & demand dashboards, please subscribe to upstream oil and gas updates from Energy Solutions.